The Super Bowl isn’t just America’s biggest sporting event—it’s the world’s most expensive marketing battleground. And in 2025, the message was clear: AI is no longer the future; it’s the present. In a year where ChatGPT, Gemini, and Llama competed not just for our attention but for market dominance, AI wasn’t just in the ads—it was the story.

It was December 2009, during my first full month living in Australia, that I penned a post commenting on the fact that Google was using broadcast (paper!) print to advertise to Britons the existence of its Chrome browser. At the time, the albeit new browser was sitting around at 3% (yes, 3%) market share versus Firefox’s 23% and Explorer at almost 60%.

How times have changed. Chrome did just fine in the end (perhaps too fine, as time will tell), and Google never did lose the broadcast advertising bug – yesterday taking part in one of the biggest broadcasts of them all.

Google clearly want to own the workspace. The tech giant used the Super Bowl to launch its “50 States, 50 Stories” campaign, showcasing how small businesses across America are leveraging Gemini within Google Workspace. The campaign features 50 businesses (including a now infamous Wisconsin Cheese Mart) – one from each state – highlighting their use of Gemini as well as Google’s commitment to supporting small businesses through AI integration.

They weren’t alone.

Super Bowl ads give us so much. One of the more valuable aspects is a snapshot of where the world’s largest economy is at when it comes to the evolution and adoption of technology. If in 1984 it was the little Mac that could, and in 2000 it was ecommerce, and if 2022 was very much the Crypto Bowl – then this year resolutely belonged to AI.

Super Bowl LIX saw a host of tech companies compete to showcase their latest artificial intelligence products.

OpenAI made its Super Bowl debut with a 60-second commercial titled “Evolution of Technology.”, using pointillism-inspired animation to depict humanity’s technological progress, from the discovery of fire and the invention of the wheel to modern AI applications like ChatGPT.

Under the direction of new CMO Kate Rouch, the ad aimed to present OpenAI’s technology as a transformative yet accessible tool for everyday life; and in doing so cement its position as the market leader in the space.

Meanwhile Meta made a play for fun and accessibility, promoting their new AI-integrated smart glasses in a spot featuring Milano alumni Chris Pratt and Chris Hemsworth, alongside Kris Jenner. The ad depicted Pratt and Hemsworth admiring then eating an expensive banana artwork in what at first, appears to be a museum.

After an eight-year hiatus from Super Bowl advertising, GoDaddy returned with a commercial promoting their AI-powered tool for small businesses, GoDaddy Airo. The ad featured actor Walton Goggins portraying various roles, emphasizing how GoDaddy Airo assists entrepreneurs in building and managing their online presence efficiently.

Taking a different approach, Perplexity AI ran a contest in which a lucky user could win $1 million. Eschewing the traditional commercial, they invited users to engage with their AI chatbot for a chance to win the jackpot. Participants were required to download the Perplexity mobile app and ask at least five questions between 1500 and 1930 PT during the game. This distinctive approach was clearly designed to more specifically boost user engagement and app downloads by leveraging the Super Bowl’s massive audience.

Whilst Perplexity seems to have taken the more direct route, all the AI advertisers in this year’s ad-fest are playing the same game – user adoption and usage of generative models and their evolving interfaces. The arms race now well underway by the owners and significant customers of LLMs may seem expensive – with a 30-second spot this year hitting a cool $8 million – but the rewards to the winners of the AI game far surpass that – just ask Google Chrome!

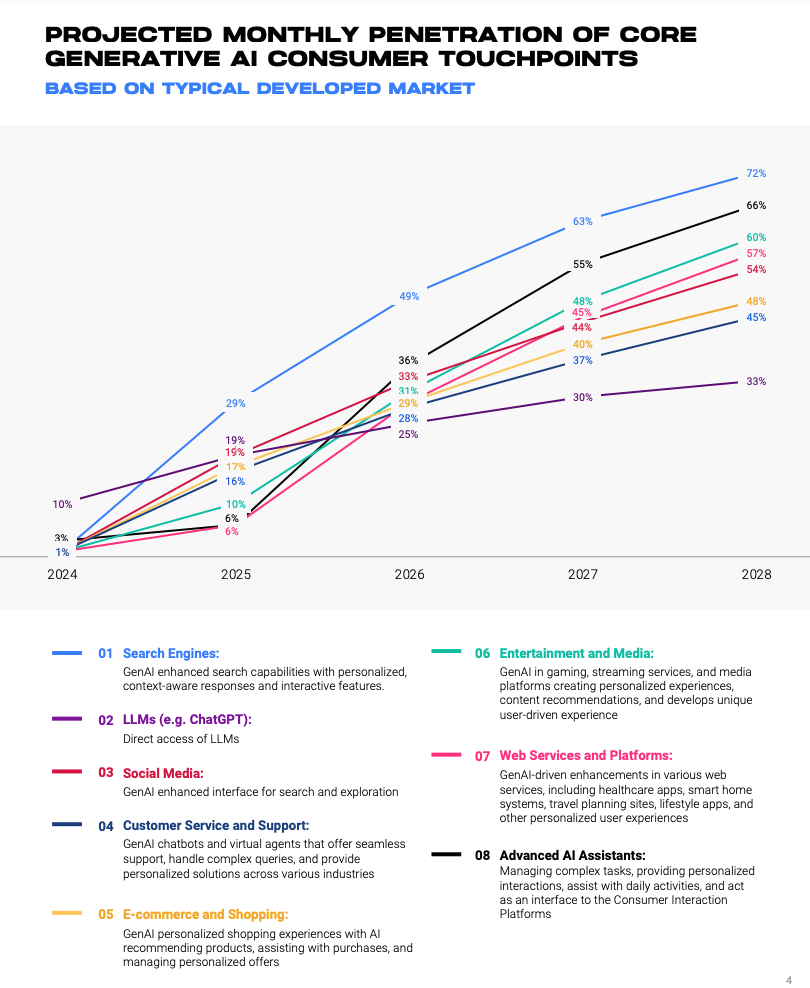

OMG projections led by the awesome JP Edwards (shout out to JP!) published in November demonstrated the huge potential for generative technologies and applications over the next three years. The Coming Wave: Generative AI (Gen AI) report projected the growth of core Gen AI services in a typical developed market from 2024 to 2028. Using expert predictions, it analysed current penetration rates, identified growth potential, and forecast key inflection points where market forces accelerate adoption.

This is the real game – and what Super Bowl LIX’s ads demonstrated was just how intense the competition is. My prediction is that whilst this year the models (Gemini, ChatGPT, Llama, Perplexity) took centre stage – by the start of 2026 we’ll be 12 months further into the Cambrian explosion of new utility now underway.

Expect next year’s Superbowl to be full to the brim not of the models, but new and emerging products and services vying for our adoption and usage. The question for brands and marketers won’t be just how they use AI – it’s how they will stand out in an AI-saturated world. Super Bowl LX won’t be about who has AI; it’ll be about who wields it best.

Buckle up people, we’re just getting started.